Zimbabwe is pursuing National Financial Inclusion Strategy 2 after what seems to have been a successful part 1. The document defines financial inclusion as ”The effective and informed use of a wide range of quality, affordable & accessible financial services by all Zimbabweans, on a sustainable basis, provided in a fair and transparent manner through formal/ regulated entities”. There’s a lot to pick from there, as there is in the 79-page long Zimbabwe_National_Financial_Inclusion_Strategy_II_2022-2026.

Financial inclusion

While the document provides the lengthy definition we have above, I’m a fan of more down-to-earth definitions. In simple terms, financial inclusion looks at how easily people can tap into formally recognised financial products and systems. This covers payments, credit access, insurance, savings, investment and digital transacting methods. This is what the financial inclusion strategy is all about, improving people’s access to financial services. With this in mind, we can look at the successes of NFIS 1 below;

increase the overall usage of formal financial services from 70% to 90%, (digital financial services from 77% to 90% transactional accounts, 15% to 50% savings, 16% to 50% credit, and 22% to 40% insurance).

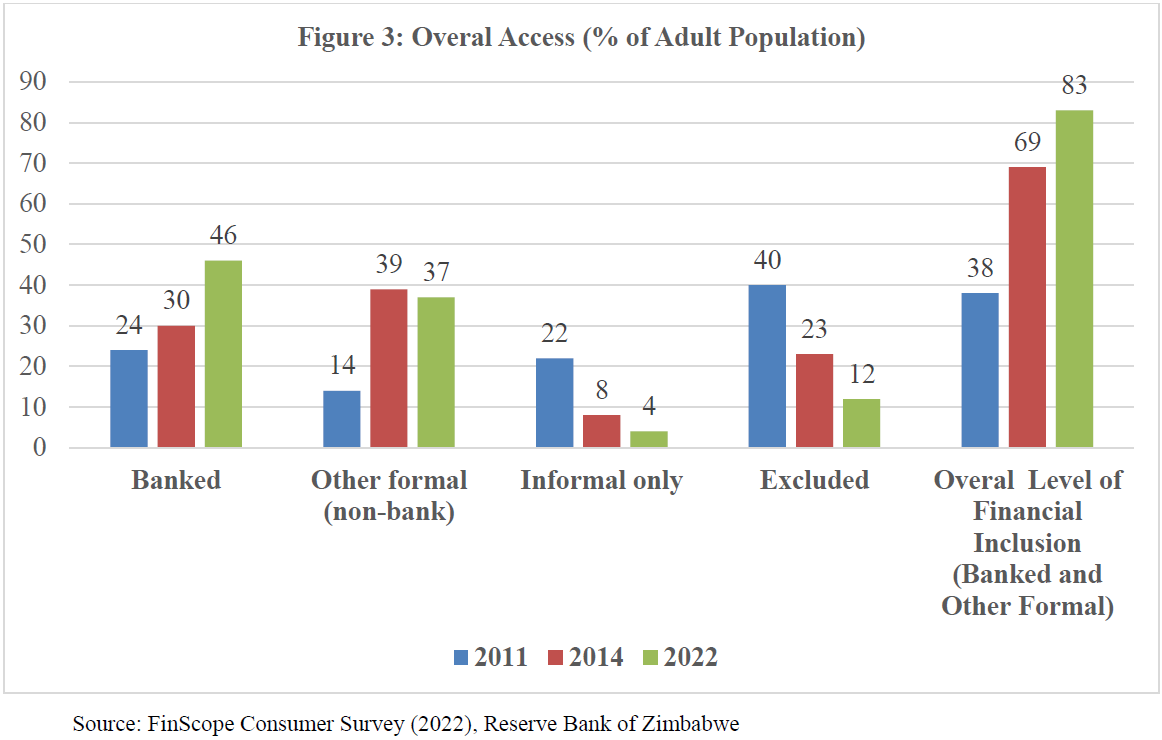

As we can see, much progress has been made in the areas of access to transacting accounts and formal banking. People using informal channels only have certainly declined, as have those who are excluded from financial access.

The raw numbers don’t tell the full story. Savings have declined from 47% to 36% since 2014. The main factors here are the overall economic downturn which has impacted incomes greatly, and the decisions in the Ministry of Finance between October 2018 and February 2019, which rendered losses in monetary value and left many people discouraged.

Mobile money usage increased from 54% in 2014 to 74% in 2022. While the report credits this to NFS1 and the Covid 19 pandemic, the reality is a cash shortage in the country has been the main proponent of this. Mobile Money accounts are as accessible today as they were in 2014. Cash is not!

The overall vision of the NFS2 is;

- Ensuring usage of financial products;

- Enhancing the range and quality of financial services and products;

NFIS 2 Outcomes

-

Financial Deepening through increased uptake and usage of quality customercentric financial products and innovative distribution channels to meet life cycle financial needs on a sustainable basis.

-

Improved livelihoods and financial capability of the target segments through sustainable usage of financial services, and a combination of knowledge, skills, attitudes and confidence to make sound financial decisions that facilitate security, resiliency, participation in economic activities, and improved quality of life.

The Outcomes of financial health are embodied in four dimensions namely

i) financial security – the ability to meet short-term commitments;

ii) financial resilience – the ability to cope with unexpected or adverse events;

iii)financial control – refers to confidence in one’s finances now and into the future

; and

iv) financial freedom – the ability to meet long-term goals and desires.

To achieve its outcomes, the document identifies specific groups that will be targeted during the years it is active. Women, youths (18-35), Persons living with disabilities (PWDs) and the elderly. However, the activities the report identifies may be useful. The 18 -35 youth group makes up 45% of Zimbabwe’s estimated 7 million adults. Roughly 52% of them are women. More importantly, we know where they are coming from as a majority (though not all) of young people revive some formal education before the age of 18. Also, a tree provides shade to everyone; a good idea is good for all involved. So let’s look at specific ideas targeted at the different groups and gain some insights.

Youth-centric financial products

This is, in part, a good idea. The youth we speak of here are the 18-35 group, as mentioned before. The struggle for the youth isn’t so much in the functionality of products but rather access to them. So heavy KYC requirements, for example, play a big part in making things difficult. However, with mobile money dominating the scene, it must be said that the major needs of youths are already met. Perhaps lite mobile money accounts are in the works?

Financial education in schools

This subject has been discussed for years, if not decades. We mentioned before that most youths would get at least some formal education before joining the 18-35 age group. So having financial education in schools is a good idea. However, let’s look at how things have shaped up in Zimbabwe, today, mobile money dominates, and I wasn’t taught that in school. Was anyone? Sadly formal education tends to trail the trend rather than lead it. Are they still teaching children about cheques?

Improved credit infrastructure

The thinking here is that improved credit infrastructure will improve access to and, therefore, the usage of credit. We’ve seen the launch of the collateral registry, which wasn’t greeted with the excitement we feel it deserves. The way traditional finance works is somewhat simple, the more certainty lenders have, the more willing they are to lend. So this is a worthy strategy to pursue to improve financial inclusion.

Designated branches for PWDs

This idea caught my eye because it is the weird combination of a good idea and a bad one at the same time. I do not speak for PWDs but rather as an observer. A branch that caters specifically to PWDs sounds a good idea when you consider how wide and varied disability is, but it also means that as a customer, one will be referred to or, in the worst case, can only use one branch of their bank. Not a great plan.

Better ideas are contained in the document, such as training and capacity building of staff and making all branches of institutions meant to serve the public friendly to PWDs. Equipping all customer-facing staff with basic sign language and disability sensitivity training would be a good start. Disability does have a wide scope, so a disability desk, as mentioned in the document, also seems a good idea.

Financial literacy – including digital financial literacy programs

There is a lot of education going on in Zimbabwe but very little financial literacy education. Even with programs that have been mentioned, such as teaching financial literacy in schools, a significant portion of the population either do not attend school or experience a bare-bones version of it. Furthermore, and rather ironically, school isn’t the best place to teach things. Children are, for the most part, just going through the motions. So programs that take advantage of the digital age are a great idea. I see a series of videos spread through WhatsApp, for example, explaining how things work.

Develop and implement innovative, inclusive financial technologies to increase the uptake and usage of financial products.

It always amazes me how kids who can’t even put their shoes on correctly can interact with Siri on an iPhone. Don’t get me started about elderly people once they learn how to send voice notes. These two things have in common how helpful technology is when applied. Developing innovative digital technologies is just what Zimbabwe needs. A banking app with a voice assistant that understands the major dialects of Shona and Ndebele? Surely that’s not asking for too much by 2026.

All in all, we can see that NFS2 is barking up the right trees. Riding on the areas where NFS1 succeeded and choosing to look at Zimbabwe as it is rather than it should be will help. One term you will see a lot of in the report is the need for disaggregated data. This means more specific data. Or data with more detail. This improves the ability to analyse the data and come up with more custom solutions for the groups involved.