It’s been in the works for months now, and recently the Reserve Bank of Zimbabwe finally launched the collateral registry. The online platform will serve as a register of collateralised moveable assets in the country. While there hasn’t been much excitement in the public sphere about this development, it does add something that the general public and business community will appreciate as time goes by. So let’s learn a little bit more about this collateral registry.

Collateral

As many should be aware by now, access to credit in Zimbabwe is complicated, to say the least. While the World Bank Ease of Doing Business Report continuously scores Zimbabwe highly in access to credit, there is some nuance to that. What is easily accessible in Zimbabwe is secured or collateralised credit; a person pledges an asset as cover if they cannot meet their repayment obligations. This makes sense as Zimbabwe is a volatile environment where fortunes can change very quickly. However, many people looking for credit do not have assets to pledge.

That said, the registry comes in to create some sanity that could improve the credit market in Zimbabwe. Including collateral, even in-person credit agreements, is perfectly legal and commonplace. The collateral registry provides a central place to register such collateral agreements, bringing two great benefits. Firstly it officialises the relationship in such an agreement and eliminates the need for lengthy legal processes for the creditor to get what is owed to them in the event of default. Secondly, it provides a central database that prevents dual or multiple collateral agreements for the same asset. Both cases are frequent in Zimbabwe, so this move is laudable.

Collateral registry

Now that we know the why, let’s talk about the what of the collateral registry. It is given legal substance in the Movable Property Security Interests Act [Chapter 14:35]. As we mentioned before, it allows people and/or businesses to register moveable property such as Livestock, household goods, crops, inventory and accounts receivable in credit agreements. On the collateral registry website, you will find a list that goes into greater detail and including;

- Agricultural products (livestock, poultry, crops etc)

- Industrial and commercial equipment

- Durable consumer goods and household items

- Agricultural equipment

- Inventory and raw materials

- Gold coins

- Accounts receivable

- Bank Accounts

- Shares

- Patents

- Copyrights and Trademarks

- Oil and Gas

- Minerals

Collateral registry website

As for the how of the collateral registry, it all happens through a website. On this website, you sign up or search the registry. This website allows people to add their entries to the website or view entries made on the website. The website search process is easy, as all you need is your name, ID Number, email address and phone number. To register for an account, you will need to upload a copy of your ID as well as supporting documents for a business or company registration. However, the website does not have site security certificates, and this is particularly worrisome for a site people enter personal data into.

The website is very thoughtful in terms of getting users accustomed to how it works and includes a user manual, user guide and even video tutorials. One area of concern I had was privacy. With uploading people’s transaction information comes a problem of people being able to find that information. The good news is that it’s not that easy. When searching the registry, you can search by ID number, Passport number or security registration number. So people cannot easily search for you by name though I can still see circumstances in which those identity document numbers may be in other people’s hands. It’s best practice to keep that information private.

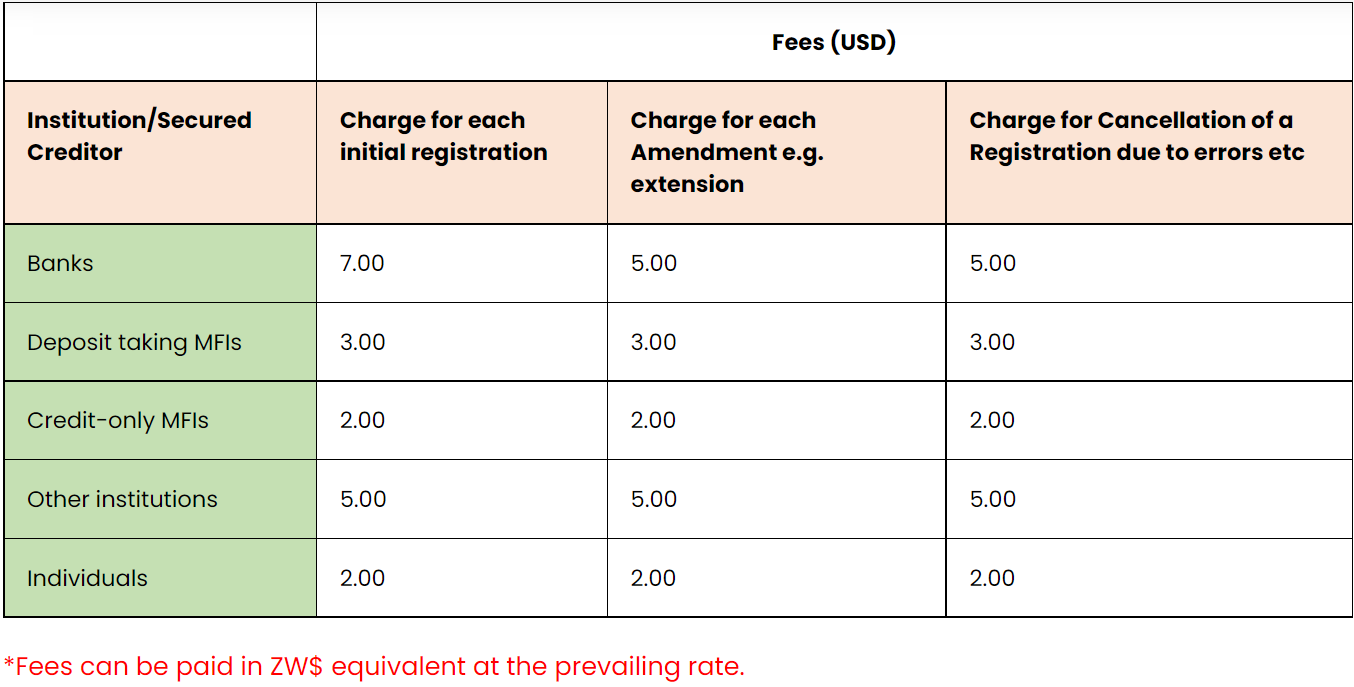

Fees

Of course, there are fees associated with the service. The fees vary depending on the identity of the fee payer. So banks, institutions and businesses will pay up to US$7 to register collateral while individuals will pay US$2. You can indicate your account type in the registration process.

The move has received a muted response for now but coupled with the National Financial Inclusion Strategy part 2 (2022-2026), which seeks to increase access to and usage of credit in Zimbabwe, it will likely make more sense in the coming years than it does now.