The sudden change in monetary law in Zimbabwe has had a shock effect on exchange rates in both markets, the interbank and parallel that is plain for all to see. The biggest in Zimbabwe remains “what is the rate”? A question that follows this one closely is of course “where is the rate going”? The latter question while not as popular is, of course, the most important.

Changing from a multicurrency to the re-rebranded Zimbabwean dollar being the sole legal tender certainly through the cat amongst the pigeons and for a while, the markets were in a state of shock and ensuing chaos. The banks were granted leeway to offer competitive rates, the parallel market temporary receded due to a reduction in demand for dollars and transaction volume coupled with an increased demand for the local currency for transacting purposes.

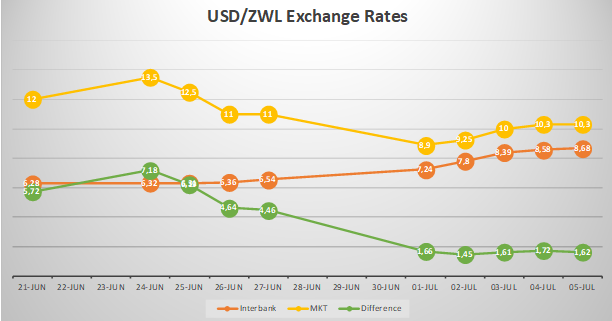

In the week following the surprise revelation of Statutory instrument 142 of 2019 the parallel market shed an estimated 35%. The interbank market rate, on the other hand, shot up significantly by roughly 10%. In some cases, the rates offered by individual banks were higher but on the condition of being an account holder with the bank or having a bank account to transfer to. In a heavily unbanked country, this doesn’t make that rate openly accessible.

With the new month of July, we have seen the parallel markets resume their upward march and rather rapidly too. Gaining an extra 16% between Monday 1st July and Thursday 4th July. The interbank market too is on an upward trend appreciating 18% in the same period.

What’s most important to note is the differential between the two markets, we have not quite witnessed the convergence of the two rates as we were told would be the case by Reserve bank of Zimbabwe Governor Dr John Mangudya, however given that the difference had peaked at 7.18 (which at the time was higher than the interbank rate at 6.32) the governor would surely take this as a win. The gap between the two markets has significantly dropped by approximately 75% in that period.

We have just started witnessing price reductions as a result of the rate though we largely witnessed price jumps as an initial reaction to the policy. I attributed the price jumps to the expectation that the rate drop witnessed was only temporary. So far this is proving to be the case. Many have questioned the logic of price reductions by entities we believed to be accessing foreign currency on the interbank market (or who sold directly in foreign currency like Simbisa Brands) when the interbank rate has actually increased.

Long story short the rate seems to be marching upward again and gaining momentum, regardless of your market of choice. What does this mean for price levels? Well, it’s likely to mean increases. Those who had rushed to reduce prices may find themselves with their tails between their legs increasing prices again. Perhaps the Reserve bank and the Ministry of Finance have another trick in their bag to halt this. We will know soon enough.