After our look at the life assurance industry, we can now look at the other side, short term insurance. Sometimes referred to as non-life insurance this is pretty much what it sounds like. It includes insurance policies with a defined term, hence the short term but it is not always short by all measures. You will find motor insurance, fire, home, contents, equipment, crops, public liability, personal accident and some natural disasters among many other types of cover. It’s easy to see how and why short term insurance is important to the business environment in any country let alone Zimbabwe.

Size of the Industry

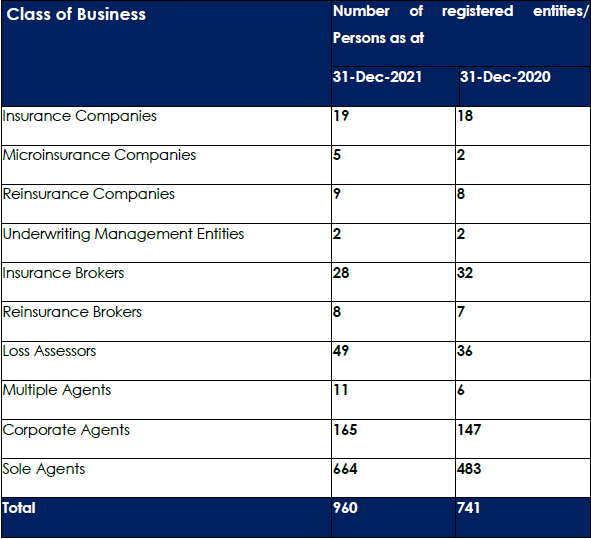

Short term insurance is a diverse industry with many players involved and a lot more business to go around. In the IPEC 4th quarter 2021 report on short term insurance in Zimbabwe, the industry comprised 960 entities registered at the end of 2021 as compared to 741 in the previous year. Notable increases were 1 additional insurance company, additional microinsurance companies and 18 additional corporate agents. Shrinkage was noted in insurance brokers and reinsurance companies. The increased diversity is a positive for the short term insurance industry.

The additions to the short term insurance industry are noted in the table below.

Motor Insurance dominates

Looking at a breakdown of the business written by short term insurance companies is dominated by motor insurance (46%). Fire insurance chipped in with 20% of the gross premium written. Other insurance includes casualty, directors liability, health and hire purchase insurance. These headline business segments have mixed performance compared to the previous year where motor insurance was up from 40% while fire insurance was down from 2% and others down from 11%. Hail insurance was the only other mover year on year, down from 5% in 2020. Foreign currency-denominated business registered a 49.87% from gross premium written of US$67.71 million to US$101.48 million owing to changes in the regulatory position on US dollar-denominated insurance policies. Major movers in this regard were hire purchase insurance which grew from zero to US$ 3 million, motor insurance which increased from US$18 799.94 to US$ 29 126 179.38 and machinery from zero to US$ 4 370 908.64.

Assets held

Due to the nature of short term insurance, the desirable investment assets for insurance companies are markedly different from that of life assurers. Investment by short term insurers is dominated by Fixed assets (31%) and Equities (23%). The fixed assets were well above the allowable limit of 10% for property which alone was 31%. In short term insurance premiums, receivables count because they can be immediately applied to any obligations that arise and they contributed to 16% of the assets of short term insurance. This is against the recommended limit of 5% The investment in prescribed assets which we explained in the article on life assurers, was only 2%, well below the recommended level of 10% for short term insurers. The investment in fixed assets which take longer to liquidate and reliance on premiums receivable is worrying for the stability of the industry.

Market share

The graph below depicts the gross premium written and net premiums written by each insurance company as a percentage of the total market for these figures. Zimnat Lion (17.4%), Nicoz Diamond (17.1%) and Old Mutual (15%) were the leaders on a gross premium written basis. The “big three” shuffled for the net premium written basis with Old mutual (19.1%) coming out on top, Nicoz Diamond with 15.7% of the market share and Zimnat Lion grabbing 12.7% of the market share. The difference between GPW and NPW is that GPW looks solely at the amount received in premiums from the customer or insured party. NPW goes further to account for costs associated with maintaining the insurance policies.

If we look at the market share based on assets invested, Old Mutual is by some way Zimbabwe’s largest insurance company. Holding just under 18% of the assets invested in by short term insurers. Not many surprises in the rest of the ranking though Alliance is nestled between Nicoz Diamond (12.1%) and Zimnat Lion (11.3%) with 11.7% of assets to break the hold of the “big three”.

For the foreign currency-denominated business we have a bit of a shakeup. Cell Insurance leads the way with 20.4% of the GPW market, their focus on motor insurance will have contributed to this. Zimnat Lion (19.6%) and Old Mutual (16%) made up the top three for GPW. In NPW Zimnat lead the way with 22.7% of the business, Cell Insurance registering 22.1% while Alliance captured 13.4% of the business.

Complaints Handling

Finally, the report looks at complaints handling in the period. A total of 22 complaints we received. 10 being for delayed settlement while the remaining 12 were repudiations. Repudiation in simple language is a situation where a breach by one party in an agreement allows another party to cancel the agreement. An example we can all relate to is when an insured party ceases to make payments for a period of say 3 months, the insurer then chooses to cancel the policy. So repudiation complaints include those where these and other similar circumstances have occurred. On the bright side, 21 of the 22 complaints were resolved with 1 repudiation complaint outstanding.

The landscape through difficult looks positive for the short term insurance industry. Regulatory changes have gone some way to justifying insuring for the market, especially the foreign currency based policies. The industry is a little more volatile as evidenced by the 4 insurance company deregistrations during the year but it is pleasing to note that all registered insurers meet capital adequacy requirements.

All images in this article were obtained from the 2021 Fourth Quarter Non-Life Industry Report